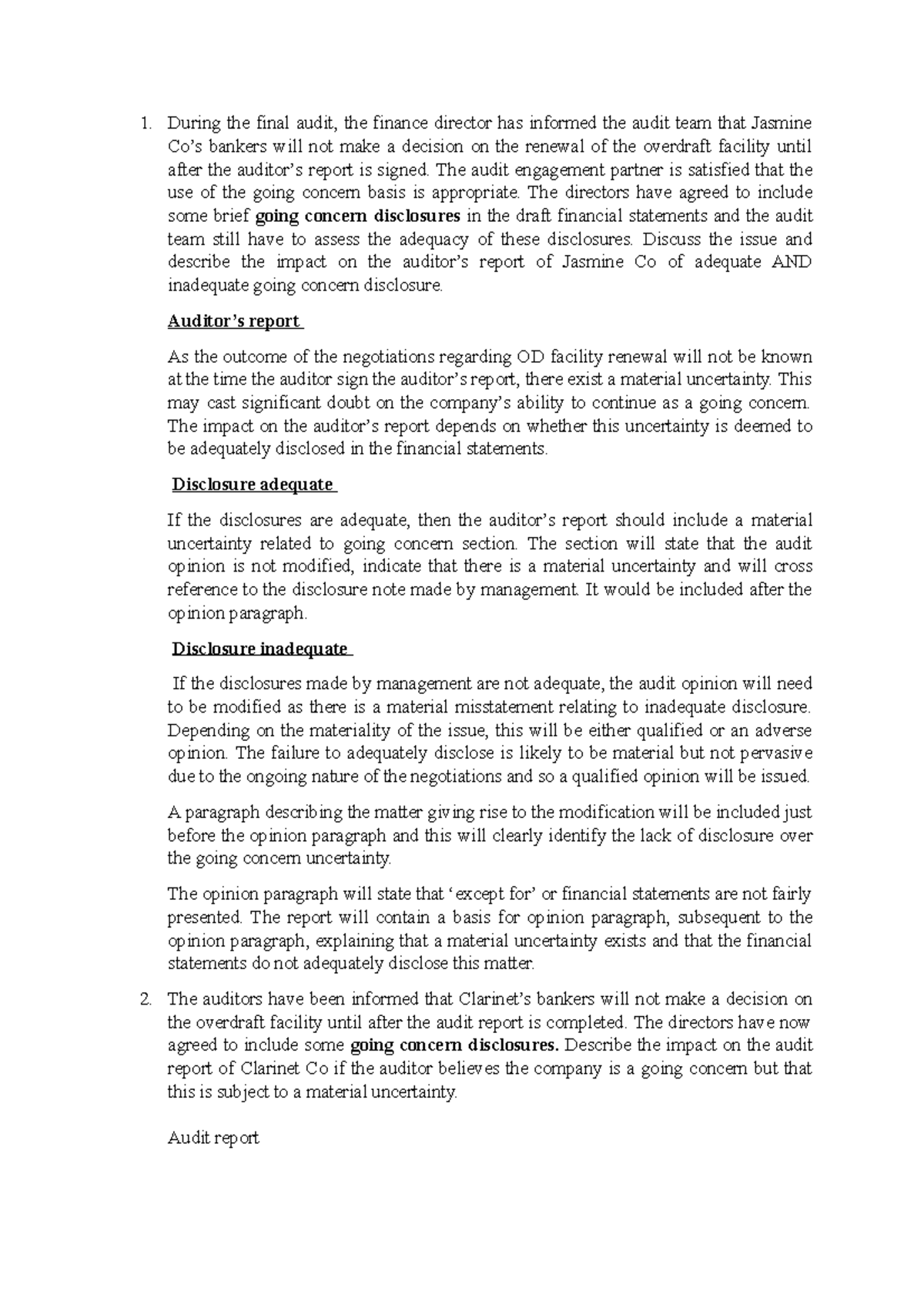

Material Uncertainty Related To Going Concern Qualified Opinion

And appropriate to provide a basis for our opinion. FMA expects the auditors of issuers to address the observed shortcomings in audit reports with respect to going concern disclosures to ensure that their performance in relation to the matters.

Pdf Analyzing The Going Concern Uncertainty During The Period Of Covid 19 Pandemic In Terms Of Independent Auditor S Reports

Material uncertainty related to Going Concern If the company adequately discloses concerns about going concern uncertainty then auditor will issue an unmodifiedunqualified opinion and a separate section called Material uncertainty related going concern aDraws attention to a Note in financial report If company doesnt disclose going concern issues then auditor issues a.

Material uncertainty related to going concern qualified opinion. As stated in Note 6 these events or conditions along with other matters as set forth in Note 6 indicate that a material uncertainty exists that may cast significant doubt on the Companys ability to continue as a going concern. Exists Revised Concern Financial. Determine whether or not a material uncertainty exists related to events or conditions that may cast significant doubt on the entitys ability to continue as a going concern hereinafter referred to as material uncertainty through performing additional audit procedures including consideration of.

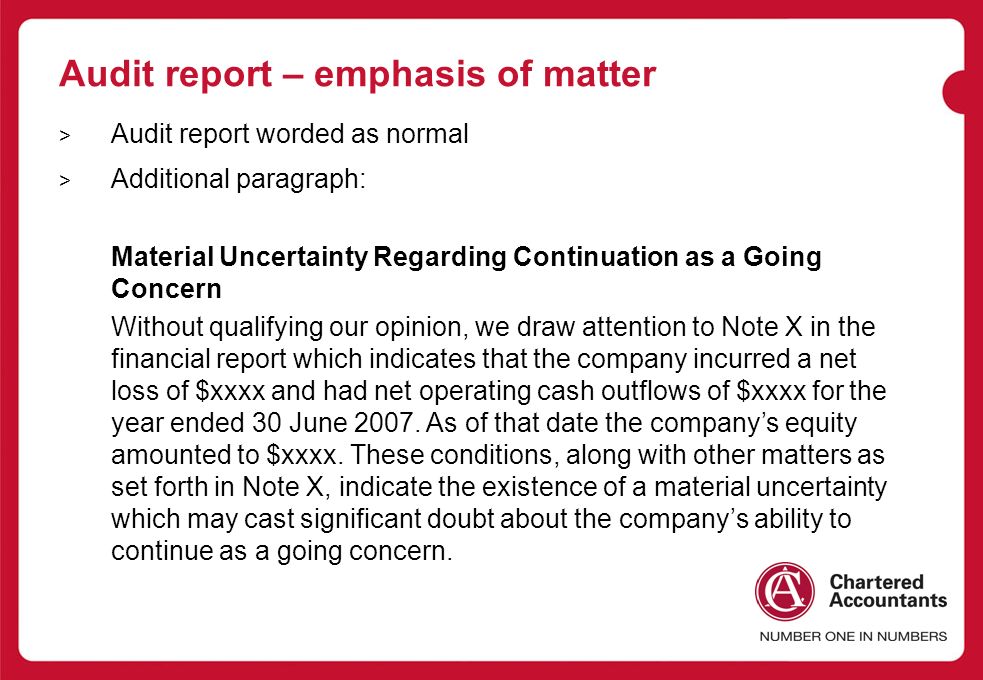

Material Uncertainty Related to Going Concern We draw attention to Note 27 to the financial statements which disclosed that the Group and the Company incurred a net loss of RM22224 million and RM13165 million respectively during the financial year ended 31 March 2020 and as of that date the Groups and the Companys current. Paragraph under the heading Material Uncertainty Related to Going Concern drawing attention to the disclosures related to the ability of the entity to continue as a going concern. Pursuant to paragraph 91937 of the Main Market Listing Requirements of Bursa Malaysia Securities Berhad the Board of JCB wishes to announce that the Companys External Auditors Messrs Grant Thornton Malaysia had expressed their qualified opinion with material uncertainty related to going concern in the Companys Audited Financial Statements for the.

Heading Material Uncertainty Related to Going Concern It is only where the auditor ncludesco that managements proposed approach to the use of the going concern basis of accounting is not appropriate or that there is insufficient disclosure about a material uncertainty that a modified opinion will arise. A matter giving rise to a opinion modifiedin accordance with ISA 705 Revised or a material uncertainty related to events or conditions that may cast significant doubt on the entitys ability to continue as a going concern in accordance with ISA 570. Paragraph 9-2 b of ISA UK 570 Revised September 2019 includes a definition of a material uncertainty related to going concern as follows.

However this is not described in detail as part of the key audit matters section and the auditor needs to refer in that section to the Material uncertainty related to going concern section of the audit report. The Group incurred loss after tax of 145879000 for the financial year ended 30 June 2019 and as at that date the Groups current liabilities exceeded its current assets by 20821000. HLB AAC PLT the Companys Independent Auditors had expressed a qualified opinion and material uncertainty related to going concern in the Companys Audited Financial Statements for the financial year ended 30 June 2021 AFS.

If it is so why the Material Uncertainty Related to Going Concern section in the new audit report is only a modified report but not an unmodified opinion. Our opinion is not modified in respect of this matter. It will also state that the auditors opinion is not modified in respect of this matter.

1223 HARD You are the audit partner at Preston Associates a midi-tier audit firm. AUDIT REPORT - MODIFIED OPINION MATERIAL UNCERTAINTY RELATED TO GOING CONCERN. AUDIT REPORT - MODIFIED OPINION MATERIAL UNCERTAINTY RELATED TO GOING CONCERN.

I believe the IAASB has not completely resolved the ambiguities involved in the new audit report. Pursuant to Paragraph 919 37 of the Main Market Listing Requirements of. An uncertainty related to events or conditions that individually or collectively may cast significant doubt on the entitys ability to continue as a going concern where the magnitude of its potential.

Introduction Pursuant to Paragraph 91937 of the Main Market Listing Requirements of Bursa. COMINTEL CORPORATION BHD Comcorp or the Company Qualified Opinion on the Audited Financial Statements for the Financial Year Ended 31 January 2020. The section headed Material Uncertainty Related to Going Concern is included immediately after the Basis for Opinion paragraph but before the KAM section.

In an audit going concern is defined as the companys ability to continue its operations for the foreseeable. Unqualified opinion with going concern. A material uncertainty.

A material uncertainty exists related to events or conditions that individually or collectively may cast significant doubt on the entitys ability to continue as a going concern. Qualified Opinion on the Audited Financial Statements for the financial year ended 31 December 2018 1. TOYO VENTURES HOLDINGS BERHAD - QUALIFIED OPINION ON THE AUDITED FINANCIAL STATEMENTS FOR THE FINANCIAL PERIOD ENDED 30 SEPTEMBER 2021.

The Material Uncertainty Related to Going Concern section will follow the Basis for Opinion paragraph and will cross-reference to the relevant disclosure in the financial statements. It should be noted that where the uncertainty is not adequately disclosed in the financial statements the auditor would continue to modify the opinion in line with ISA 705 Modifications to the Opinion in the Independent. Occur the material uncertainty related to those events or conditions and the plans in place to address those uncertainties must be improved.

Material uncertainty related to going concern We draw attention to Note 21 to the financial statements. Modified audit opinion or qualified independent examiners report on making a modified audit opinion emphasis of matter material uncertainty related to going concern or issuing of a qualified independent examiners report identifying matters of concern to which attention is drawn notification of the nature of the modification. I Where the use of the going concern basis is not appropriate the auditor.

You are responsible for the audits of the following three independent entities for the year ended 30 June 2018. If the auditor reports on key audit matters any material uncertainty related to going concern is by its nature a key audit matter. Pursuant to Paragraph 919 37 of the Main Market Listing Requirements.

Related party transactions etc. Audit Report - Modified Opinion Material Uncertainty Related to Going Concern Qualified Opinion Description. The Board of Directors of the Company wishes to announce that Messrs.

Impact Of Covid 19 On Going Concern Assessments

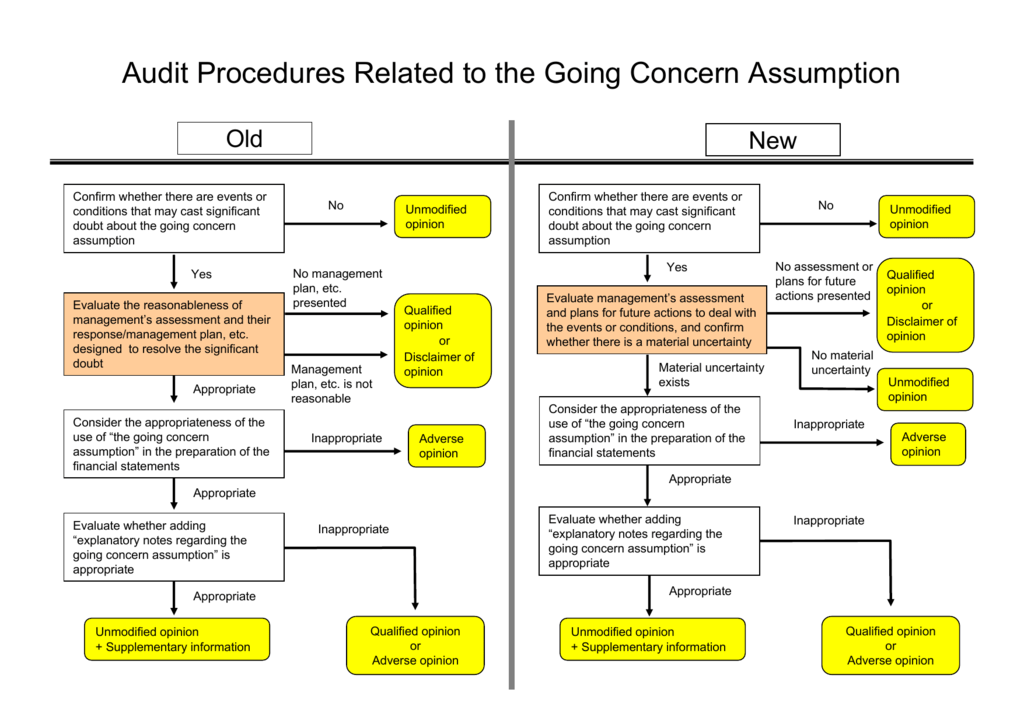

Audit Procedures Related To The Going Concern Assumption Pdf

Going Concern Consolidated Previous Quest Answers Pattern Without Studocu

Chartered Accountants Audit Conference Problem Audit Reports Charteredaccountants Com Au Andrew Stringer Head Of Audit The Institute Of Chartered Accountants Ppt Download

2

{kind=link}

Posting Komentar untuk "Material Uncertainty Related To Going Concern Qualified Opinion"